MicroStrategy has transformed itself from a traditional software company into a Bitcoin proxy. Over the past years, the company has consistently bought $Bitcoin, often using debt, convertible notes, and equity offerings to do so.

As a result, Bitcoin now dominates MicroStrategy’s balance sheet. The company holds hundreds of thousands of BTC, making its valuation highly sensitive to Bitcoin price movements. This strategy works extremely well during bull markets — but it also creates structural risk during prolonged downturns.

At this point, MicroStrategy is no longer just “exposed” to Bitcoin. It is financially tied to it.

Bitcoin remains the key variable in MicroStrategy’s future.

Looking at the attached weekly $BTC chart:

- Bitcoin recently lost momentum after failing to hold above major resistance

- Current price action is hovering around a critical support zone

- Momentum indicators remain weak, suggesting continued downside risk

BTC/USD 1W – TradingView

While Bitcoin has historically recovered after deep bear markets, those recoveries often came after long periods of stagnation. In previous cycles, BTC spent one to two years moving sideways or declining before resuming its uptrend.

A scenario where Bitcoin drops sharply — or even trades at depressed levels for years — cannot be ruled out.

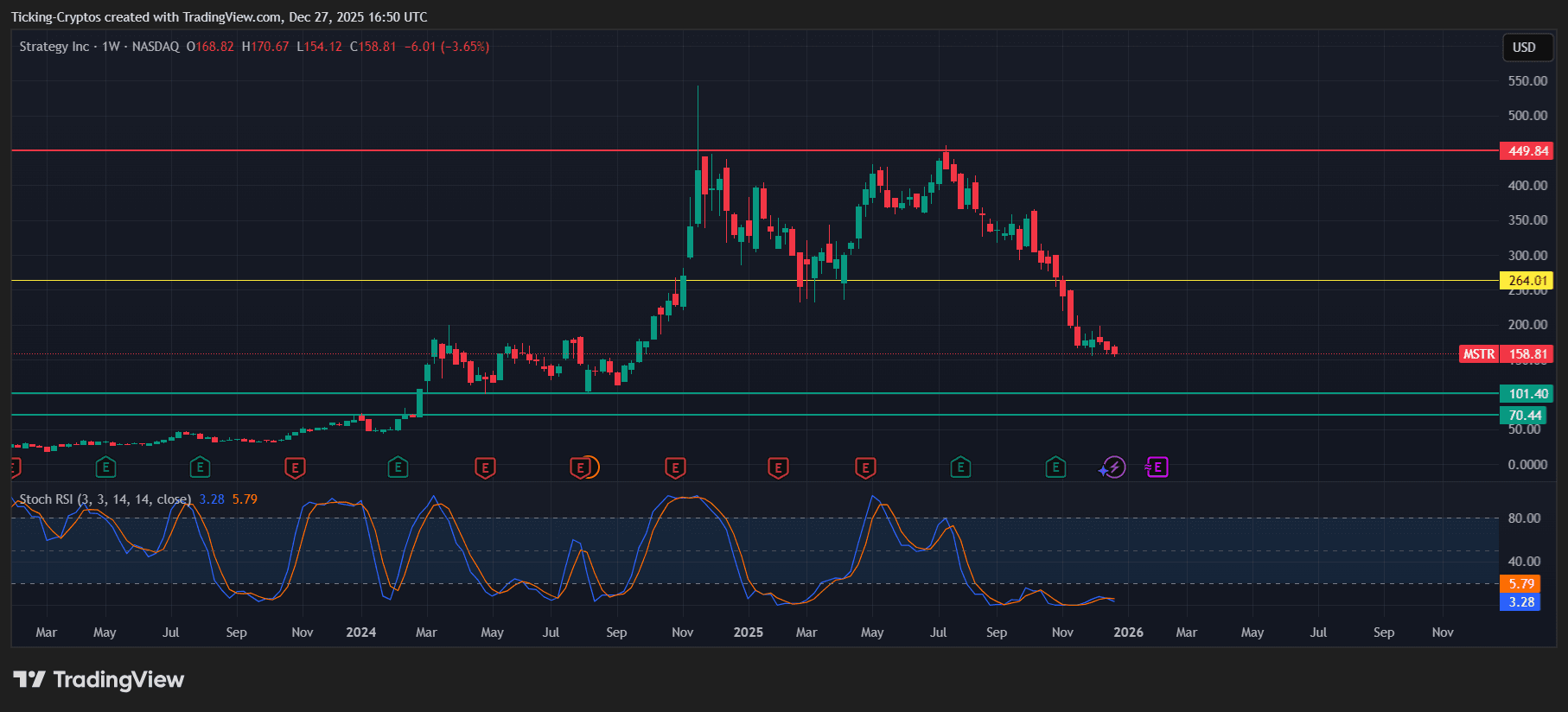

MicroStrategy Stock Analysis: Leverage Cuts Both Ways

The MicroStrategy chart reflects this risk clearly.

- MSTR peaked near major resistance and has since entered a strong downtrend

- Key support levels have already been lost

- The stock is now trading far below its highs, mirroring Bitcoin’s weakness

MSTR 1W – TradingView

While MicroStrategy does not move tick-for-tick with Bitcoin, the correlation increases sharply during market stress. When BTC sells off aggressively, MSTR tends to underperform due to leverage, debt exposure, and investor fear.

In bull markets, MSTR often outperforms Bitcoin. In bear markets, it typically falls harder.

Are Bitcoin and MicroStrategy Fully Correlated?

Not entirely — but close enough to matter.

Bitcoin determines:

- The value of MicroStrategy’s reserves

- Investor confidence in its strategy

- The company’s ability to raise capital cheaply

MicroStrategy, however, also carries:

- Operating costs

- Employee salaries

- Debt servicing obligations

- Corporate expenses unrelated to Bitcoin price

Bitcoin can afford to “do nothing” for years.

A company cannot.

The Structural Problem: Time Works Against Companies

Bitcoin could theoretically crash toward zero, stay there for two years, and later recover. It has no payroll, no debt payments, and no operational burn.

MicroStrategy does.

If Bitcoin were to:

- Remain deeply depressed for multiple years

- Trigger large unrealized losses on the balance sheet

- Limit access to new financing

Then MicroStrategy could face serious sustainability issues, regardless of long-term Bitcoin optimism.

This is not about belief in Bitcoin — it is about corporate survivability under prolonged stress.

A crash is not guaranteed, but the risk is real.

MicroStrategy’s future depends heavily on:

- Bitcoin holding long-term value

- Avoiding extended multi-year drawdowns

- Maintaining access to capital markets

If Bitcoin recovers quickly, MicroStrategy benefits massively.

If Bitcoin enters a long, deep winter, MicroStrategy carries far more risk than Bitcoin itself.

In simple terms:

- Bitcoin can wait

- MicroStrategy cannot wait forever

That asymmetry is the core risk investors must understand heading into 2026.